Ray Dalio, Citrini and the KOSPI's Plunge

[Opinion] Normalcy is what we both need, and must avoid, if this age of AI is to continue without a hiccup

Good Evening from Taipei,

South Korea’s benchmark equity index had a bad day. Trading in Seoul was suspended for 20 minutes late morning on Wednesday after the KOSPI index dropped to a level that was 8% below the previous day’s close, and it stayed there for at least one minute — triggering a Level 1 Circuit Breaker. Stocks kept sinking after the break, ending 12% lower for the worst daily drop since the global financial crisis of 2008.

The US-Israel war against Iran was cited as the cause: logical. Oil prices shot up after the aerial attack on the major oil producer began on 28 February: of course. South Korea imports most of its energy, thus higher oil prices are bad for its economy: probably. Meanwhile, shares of Korean defense makers like Hanhwa Aerospace have surged since the bombardment began: naturally.1

Iran’s targeting of oil tankers certainly makes the supply of energy less secure, and no electricity means no chips. But US President Donald Trump countered by offering to insure ships and protect them with the might of the US military, so that risk is surely ameliorated.

This from Investing.com’s Ambar Warrick summarize what happened:

”Wednesday’s losses saw the KOSPI wipe out as much as 18% from a record high hit last week. The KOSPI also effectively halved its year-to-date gains to around 20% on Wednesday,” Warrick wrote in a mid-morning update. “Declines were driven chiefly by profit-taking, as investors locked in recent gains and turned largely risk-averse with the outbreak of the U.S.-Iran war over the weekend.”

This one line in particular stood out: The KOSPI also effectively halved its year-to-date gains to around 20%. We’re barely two months into the year and an entire equity index, with a market cap of around $3 trillion, had already advanced 40%.

But none of the above explains why the KOSPI, which is heavily weighted toward memory-chip makers Samsung Electronics and SK Hynix, should plummet. Higher energy prices would have minimal impact on the cost of making memory chips since the biggest expense is the depreciation of their multi-billion dollar fabs. Besides, any increase could easily be passed on to customers such as Nvidia, Apple, and Dell which reportedly have teams camped out in South Korea to secure DRAM supply.

Citrini and the Global Intelligence Crisis

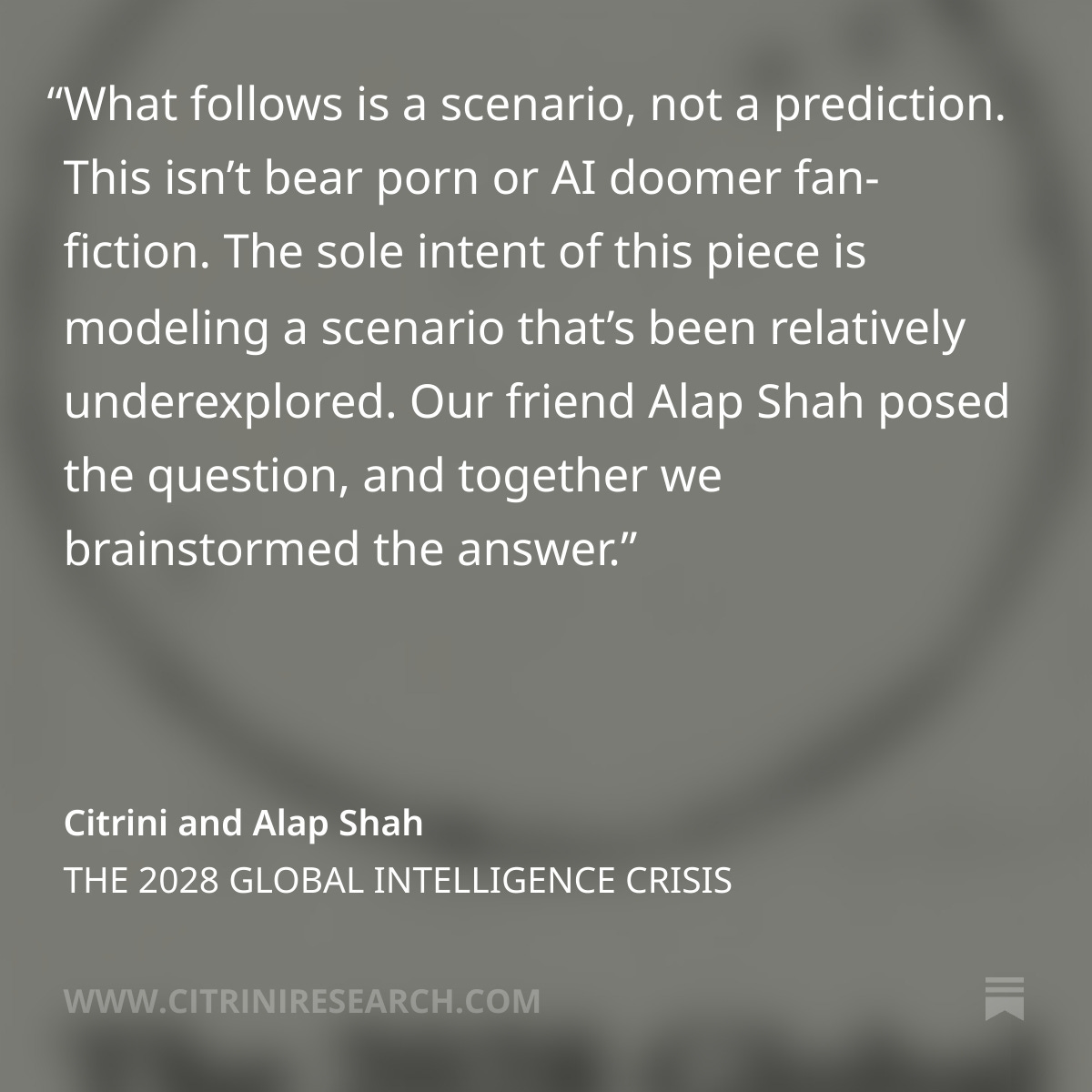

I think a good lens through which to look at this is the one offered by Citrini a few weeks ago in that now infamous report titled “The 2028 Global Intelligence Crisis.”

Citrini laid out a scenario of what the future might look like in the age of AI, it wasn’t a prediction or prescription. It was an idea.

Despite the clear explanation at the very top of the article, AI permabulls were enraged. The most common criticism it attracted was that it was “AI slop,” the internet’s insult du jour — a modern day version of “fake news.” If you don’t like something or it offends your senses, just call it AI slop.

The hate for that piece is also somewhat illogical. If Citrini’s article was the reason why billions of dollars of market cap were wiped off stocks, as has been alleged, then the weakness in the bull case is all the more apparent.

Yet, if the Citrini scenario was actually weak and fanciful, then it defies logic that such “AI slop” could possibly have such an impact on markets. For sure, traders and investors who manage billions of dollars in funds aren’t always perfectly logical, but they’re not stupid either. If Citrini’s apocalyptic scenario was entirely ill-conceived, then it would have just been ignored by most market players. The problem is that the article’s critics are so adamant that they’re smarter than the thousands of people who trade every day that they’re likely to miss the true signs of trouble when they appear.

This week’s sell off in Korean memory stocks offers another chance to check our assumptions about the AI rollout. And it’s a good time to re-examine Citrini’s essay. Here’s Culpium’s summary of Citrini’s “The 2028 Global Intelligence Crisis.”

Much of modern white-collar work deals with removing friction.

AI can remove friction more efficiently: booking flights, tax prep.

AI also makes it easier to deploy new features, removing differentiation.

No friction plus no differentiation means lower prices and fewer human jobs.

Reducing the number of humans with salaries also reduces spending power.

Economic malaise ensues.

Many of the wiser critics drilled down to specific arguments, specific scenarios, and specific case studies to prove their point. That’s exactly the way to approach it, but doesn’t necessarily deliver a knock out blow.

The best critique of the piece came from Ben Thompson at Stratechery, which probably isn’t surprising. Thompson is the father of Aggregation Theory, so naturally he homed in on the example of DoorDash. In his view, Citrini’s idea about the coming collapse of DoorDash shows that the author doesn’t really understand how these platforms work, as laid out in Aggregation Theory. Thompson might be right. He also might be wrong. I guess we’ll know if DoorDash is still around a decade from now (Citrini posited 2028, but that seems a little rushed).

Whichever way it plays out for DoorDash, Citrini’s broader argument about the possible impact AI may have on white-collar work — especially that which is dedicated to smoothing out frictions and product differentiation — remains worthy of consideration. Unfortunately for the author, they may have chosen the wrong example and argued it in a way that didn’t pass the Ben Thompson smell test.

Bubbles and Being Broadly Right

I think it’s possible to be right more broadly, even if you’re wrong on specifics.

Bubbles are the best example I can think of to illustrate this point. The collapse of the housing bubble almost 20 years ago was obvious in hindsight, but few people predicted it back then and even fewer nailed the timing. Michael Burry, immortalized in Michael Lewis’s book “The Big Short,” predicted the subprime crisis. But the tension over timing is key to the drama, and to the perception of being right.

“I may be early, but i’m not wrong,” Burry is quoted as saying. But few remember the rebuttal he received: “It’s the same thing, Michael.” In the end, Burry’s overarching thesis was right, and his timing was close enough. The bulls got crushed.

Citrini’s broader thesis is that AI will eliminate white-collar jobs, which will in turn decimate the consumer economy upon which the US and many other nations are built.

“The velocity of money flatlined. The human-centric consumer economy, 70% of GDP at the time, withered. We probably could have figured this out sooner if we just asked how much money machines spend on discretionary goods. (Hint: it’s zero.)” — “The 2028 Global Intelligence Crisis”

That’s not a ridiculous notion. Just last week Jack Dorsey laid off 40% of his workforce at Block — 4,000 people in total — and cited AI as the reason. “We're already seeing that the intelligence tools we’re creating and using, paired with smaller and flatter teams, are enabling a new way of working,” Dorsey wrote on Twitter, the very platform he founded (and which Elon Musk renamed X). It’s entirely possible he was using AI as an excuse, not a reason, but that alone proves Citrini’s point: AI will be the cover executives needed to cut staff.

This brings me to the key issue which ties Citrini and the KOSPI together.

Three months ago I argued that the 2000 dot-com bust isn’t quite the right framework from which to view the current AI rollout. Instead, I believe that the development, production, and sale of memory-chips is a more apt example. My reasoning is thus: the cost of building the factories to make the product keeps getting more expensive, yet the product being made is barely distinguishable from rivals (it’s a commodity), and the price is constantly falling. Thus, AI tokens and memory chips are largely similar.

Right now, the price of DRAM chips is rising thanks to the current AI boom which is stealing capacity from traditional uses such as computers and smartphones. This won’t last. In fact, the usual trend of falling ASPs (per bit) will resume because clients demand it and suppliers will be able to deliver it. We’re in a short-term anomally, not long-term stasis. These companies will lose money one day, because the industry is so cyclical that booms always turn to busts.

Normalcy is Bad News

One reason why the KOSPI took a tumble this week is because that return to normal may be closer than we’d previously expected. Not so much because of an immediate cut in demand for DRAM, or even a lowering of the short- to long-term view of the AI rollout, but because what underpins all of this is the broader global economy.

Higher oil prices tend to boost inflation while also lowering economic activity. Data also shows that capital investment suffers during such periods. MSCI this week modeled a scenario where a 35% rise in oil prices resulted in a 13% drop in US equities.

Current massive capex budgets by major technology companies, from Amazon.com and Alphabet, to Meta and Microsoft, is only possible because they’re sitting on legacy cash-cow businesses. These are driven by discretionary spending and monetized through volatile businesses such as ads, software & cloud-services, and e-commerce. This cash needs to keep flowing because the gargantuan sums they’re burning on AI infrastructure is years away from turning a profit. Any threat to that money stream threatens their ability to keep buying expensive Nvidia chips, and the high-bandwidth memory produced by Samsung and SK Hynix.

Yet the Citrini scenario also applies. Capex, once spent, cannot be unspent. AI data centers are a drag on income for five to seven years, at a minimum, and up to 20 years for the building and plumbing. If AI truly does allow a company to do more with fewer staff, then there’s no reason not to do a Dorsey and fire people. Investment figures, one of the components of GDP, could continue to rise even as unemployment climbs — creating what Citrini calls “Ghost GDP.” Additionally, any uncertainty gives executives great cover to cut staff by blaming the economy — indeed, it almost compels them to do so.

On the flipside, however, economic uncertainty also compels executives to be a little more circumspect in how much they spend on future AI infrastructure. Past capex can’t be undone, but future earnings can be saved by rolling back or delaying their pending equipment purchases. I am not saying that’s what’s happening now, in fact I have seen no evidence yet that it is. But a savvy investor would be wise to price it in to their model given the uncertainty surrounding the current Middle East conflict which has already impacted flights and threatened maritime transport.

Ray Dalio and the Arenas of Conflict

There’s a third aspect that’s also worthy of attention. A few weeks ago Ray Dalio made the bold proclamation “It’s Official: The World Order Has Broken Down.” While he was being a little hyperbolic, Dalio’s comment on Twitter was actually a distillation of statements made by world leaders at the Munich Security Conference. His claim wasn’t entirely clickbait.

Dalio then followed up by generously copy-pasting Chapter 6 of his best-selling book “Principles for Dealing with the Changing World Order.” That chapter, titled “The Big Cycle of External Order and Disorder” is a walk through the history of the causes of war and strife, in which he presents his thesis on the five major kinds of fights between countries, and how each are connected to the other.

One particular passage struck me, and I’m reminded of it today as I look at Citrini’s thesis and the KOSPI’s plunge:

“The United States and China are in an economic war that could conceivably evolve into a military war,” Ray Dalio wrote, noting that technology is among the arenas in which nations fight. And he goes onto observe, and perhaps warn, that “protecting one’s wealth in times of war is difficult.”

The AI permabulls are convinced that artificial intelligence will upend the world, and they may be right. If they’re wrong, then being cautious about massive capex and continued demand for expensive GPUs and precious memory chips is warranted. If they’re correct, however, the possibility of this technology upending economies and nations is also high.

Surely, then, there’s wisdom in “protecting one’s wealth” in this time of war.

Thanks for reading.

More From Culpium:

They did take a dive Wednesday, after a massive run up in prior days.