Inside Apple's Chipflation Dilemma

[Exclusive] The iPhone maker is facing unprecedented cost expansion, with memory jumping to become the single-largest cost item.

Good Evening from Taipei,

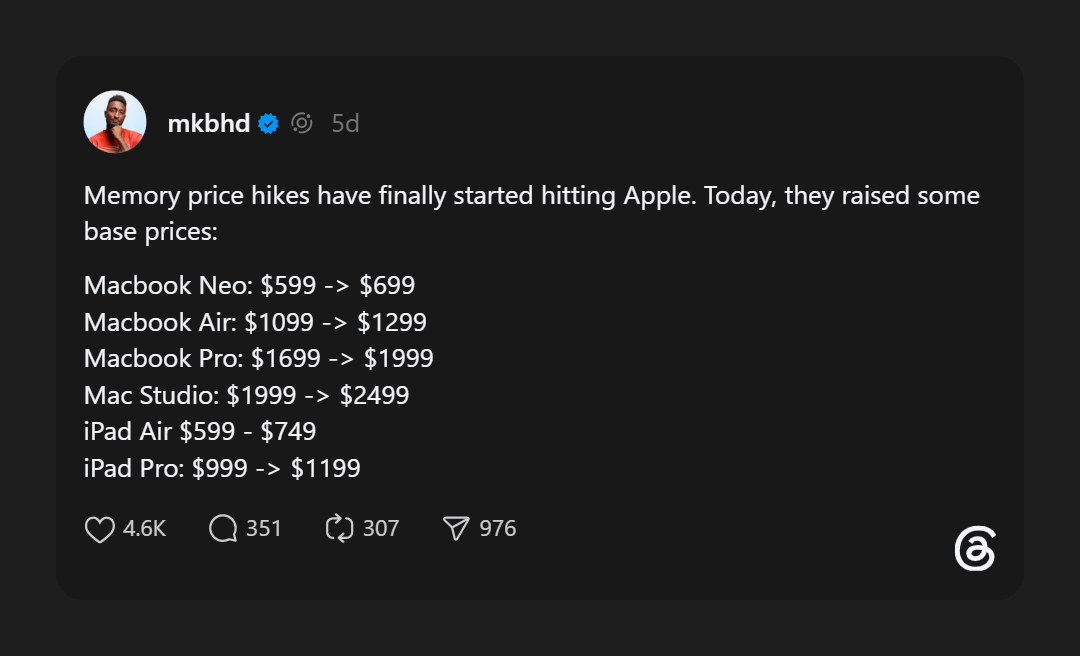

Apple’s decision to raise prices across the board last week took a lot of people by surprise. Customers rued their decision to hold off buying a new MacBook Neo or MacBook Pro after seeing costs jump.

Many also saw it as another example of Apple flexing its pricing power, convinced that consumers will still buy no matter how much Cupertino charges.

It’s the exact opposite.

It was an admission of defeat. Proof that decades of strict supply-chain discipline and buying power no longer hold up.

Apple had tried for months to save money, my sources tell me. But skyrocketing DRAM costs have driven the price of memory from $30 per phone to over $130 apiece, bringing it above 30% of the cost of building an iPhone, according to my discussions with sources.

In reality, Apple’s decision to add $100 to a MacBook Neo, $300 to a MacBook Pro, and $500 to a Mac Studio shows Apple’s waning position in the global supply chain for technology hardware.

The hikes also reveal the company’s Achilles’ heel, where Tim Cook and his team have minimal bargaining power.

Regular readers of Culpium have watched me map out this change over the past six months.

In January I wrote that Apple is Fighting for TSMC Capacity as Nvidia Takes Center Stage.

“The iPhone maker’s chip designs are no longer guaranteed a place among TSMC’s almost two dozen fabs. What (CEO CC) Wei probably didn’t tell Cook is that Apple may no longer be his largest client.” — Culpium, 15 January 2026.

Then, in February, I shared that TSMC’s N2 Node is Almost Booked Out for the Next Two Years. The ongoing struggle for TSMC capacity “came to light during the Covid pandemic when car makers were caught short. The current situation, however, is more acute than ever.”

Happy Conundrum

By happenstance, Apple soon found itself caught in an interesting conundrum. In April I wrote that it was running out of the binned chips used in the MacBook Neo and was considering whether to order more. “If they do proceed with a fresh order … then it will most likely need to raise prices of the MacBook Neo.” A big part of that higher cost, I explained at the time, was the likely need to pay more for its A18 Pro processors.

Apple did end up ordering that fresh batch, and in May I explained that pricier logic chips weren’t the only challenge in keeping a lid on costs. “DRAM prices have escalated since the initial production run, driving the Neo’s bill of materials much higher.”

And if all of that wasn’t enough of a hint, there was my very blunt assessment that Memory Makers Are Strangling the Rest of the Tech Industry. “SK Hynix didn’t sell more DRAM, it just charged more for it,” I wrote in April.

So in that context we can see that Apple’s price hike last week was not sudden, it was not rash, and it wasn’t Tim Cook displaying some fit of pique.

It was calculated, planned, and executed over a period of months. Apple could see it coming as far back as six months ago, my sources tell me, and has been preparing the groundwork ever since.

And the messaging was carefully stage managed.

First was the timing. Cook, as CEO, or his CFO Kevan Parekh could have signaled the price rise back in its April 30 earnings call, or they could have done so in the next event around a month from now. But they chose the end of June, when the message wouldn’t get lost.

Then they chose the medium. In this case, an interview with The Wall Street Journal’s Rolfe Winkler, the same reporter who got exclusive tours of Apple supplier facilities including TSMC, Foxconn, and GlobalWafers back in February.

To be clear, I am not dissing Winkler for getting an interview with Cook and being a conduit for Apple’s message. I have conversed with Winkler many times, he has quoted me in his pieces, and I find him to be a very diligent journalist. In fact, I know from first-hand experience that any interview with an Apple executive will yield little beyond the exact message Apple wants conveyed.

And so it was in that interview that Cook softened the ground for what would come next.

“The main point is unfortunately price increases are unavoidable. We’re doing our best to mitigate the huge increases that are being passed to us,” Cook told the WSJ.

That point about mitigating price increases is not just PR fluff aimed at making us feel sorry for the company — although that’s part of it.

The truth is, my sources tell me, Apple has been pushing its supply chain hard over the past six to 12 months to save pennies and pounds. But the inflationary winds are stronger than even Mighty Apple can bear.

Eat the Cost

Apple could, theoretically, eat the cost and suffer lower margins as a result. But come on, it’s a publicly listed company whose $4 trillion value derives from a combination of cult-like following and the fattest margins in consumer electronics.

Within days of that WSJ interview came the price rise. And with it the blame game.

Listen to Jon Y from Asianometry and myself discuss how memory-makers ignored the coming AI boom in this episode of Supply-Chained.

Memory chips aren’t the only thing that’s become more expensive over the past year. We already know that logic chips have gone up in price, which includes not only core A-series and M-series processors but also microcontrollers, power-management, networking, and display drivers. There’s also upward pressure on magnets, exterior casings, and even batteries.

But Cook chose to blame memory.

“There’s less supply at a time when consumers want devices and the memory guys are passing along huge price increases …. We definitely need memory pricing and supply to return to reasonable levels for consumer products. That’s the bottom line.” — Apple CEO Tim Cook, WSJ 17 June 2026.

Memory takes the rap for two reasons. It’s the component he has the least control over. More importantly, according to my discussions across the supply chain, memory’s contribution to Apple’s total components costs will climb to as much as one-third of the bill of materials for many devices during calendar 2026. And Cook could do nothing to stop it.

What’s different about memory is Apple’s minuscule position in that market. Apple can, and has, bullied display makers into cutting OLED prices, keeping battery costs under control, and squeezing more out of camera-lens suppliers. That’s because in most cases it’s one of, if not the, largest customer.

For dozens of companies the calculus is stark: lose Apple and you lose a huge slice of your business. The corporate graveyard is full of suppliers who once leant too heavily on Apple. If you’re lucky the company will buy you out. Unlucky and you’ll face bankruptcy.

A major criticism leveled at Apple in the past week is that the company turned the screws on memory makers for years, and this price increase is its comeuppance. But that’s not quite how it works, especially in DRAM.

Lack of Leverage

Apple has very little leverage over memory-chip makers. The company was once famous for buying up NAND because at the time the iPod was the single-largest use for this relatively expensive storage solution. Today, NAND is the primary storage in both laptops and smartphones, and Apple has a minor share in both.

Lenovo, Dell, and HP are the global leaders in personal computers, with each putting roughly the same amount of DRAM and NAND into their products as go into any flavor of Mac. And at roughly 20% global smartphone share, the iPhone has no monopsony power over Samsung, SK Hynix or Micron. There’s also the mammoth amounts of memory buzzing away in data centers across the globe dishing out Netflix shows, Spotify streams, and Substack feeds.

As a result, Apple is nowhere near the largest buyer of DRAM and has a dwindling share of NAND purchases.

Memory makers will neither dine out nor go bankrupt on the basis of Apple orders.

To the big three, Apple is just another customer. As proof, witness Micron’s recent announcement that it has signed 16 Strategic Customer Agreements (SCAs) “across the data center, consumer and auto market segments.” My sources tell me that cloud-service providers are a major component of this SCA roster, an indication that end-customers are getting more involved in the purchasing deals that were once left to manufacturing partners like Foxconn, Wistron, and Flex.

Crocodile Tears

Yet Micron is crying crocodile tears, referencing the last memory downturn as proof of its downtrodden status.

“We told a couple of the customers who were being very aggressive with pricing at that time that this is not constructive,” Micron Chief Business Officer Sumit Sadana told the WSJ. “A lot of the industry investments got shut down in 2023 because of really poor pricing and really poor margins.”

Many, including the WSJ, figured Sadana was talking about Apple, even though he didn’t name the company directly.

I don’t know whom he was referencing, but there’s a few things worth noting. The most obvious: he said “a couple.” So, Apple isn’t solely responsible, if at all. Second, as I explained above, Apple simply does not have enough sway to depress Micron’s capex plans if there’s enough market-wide demand to justify expansion.

Which brings me to another important point. While Micron recently signed over a dozen SCAs, Apple is also putting its own balance sheet to work by making advanced payments to the Boise, Idaho-based company to help its expansion in New York.

What’s more, Micron blaming the last downturn for failure to expand now is utterly nonsensical. ChatGPT came out in 2022 and within months it was clear that AI had ignited a computing-hardware boom. As early as May 2023, in a previous life, I wrote that Nvidia isn’t the only one getting a massive AI boost. It was clear to me, a humble journalist, that memory demand was about to take off.

To blame Apple, a minor buyer of a commodity product in the middle of a boom in which Apple has played almost no part reeks of hypocrisy, stupidity, and fear. Yes, fear.

As much as we all want to blame Apple, the truth is Micron and its fellow oligopolists are enjoying stratospheric price hikes without having made the capacity investments needed to meet the demand of an epoch-defining moment. That doesn’t make them downtrodden, that makes them antitrust targets.

At the same time, raising prices doesn’t help Apple sell more products in an era of tepid smartphone and PC growth. Many people want to label Apple a bully. It’s certainly earnt that label for its actions over the past quarter century. But that was then, and we’re in a new era.

Apple didn’t raise prices because it’s a bully, it did so because it’s no longer a bully. In fact, Apple is starting to look like the opposite: an insecure kid struggling to remain relevant in a global supply chain that’s found another schoolyard king.

Thanks for reading.