Memory Makers Are Strangling the Rest of the Tech Industry

[Opinion] The AI sector will finally get the chips it needs, but everyone else will continue hurting for years to come

Good Evening from Taipei,

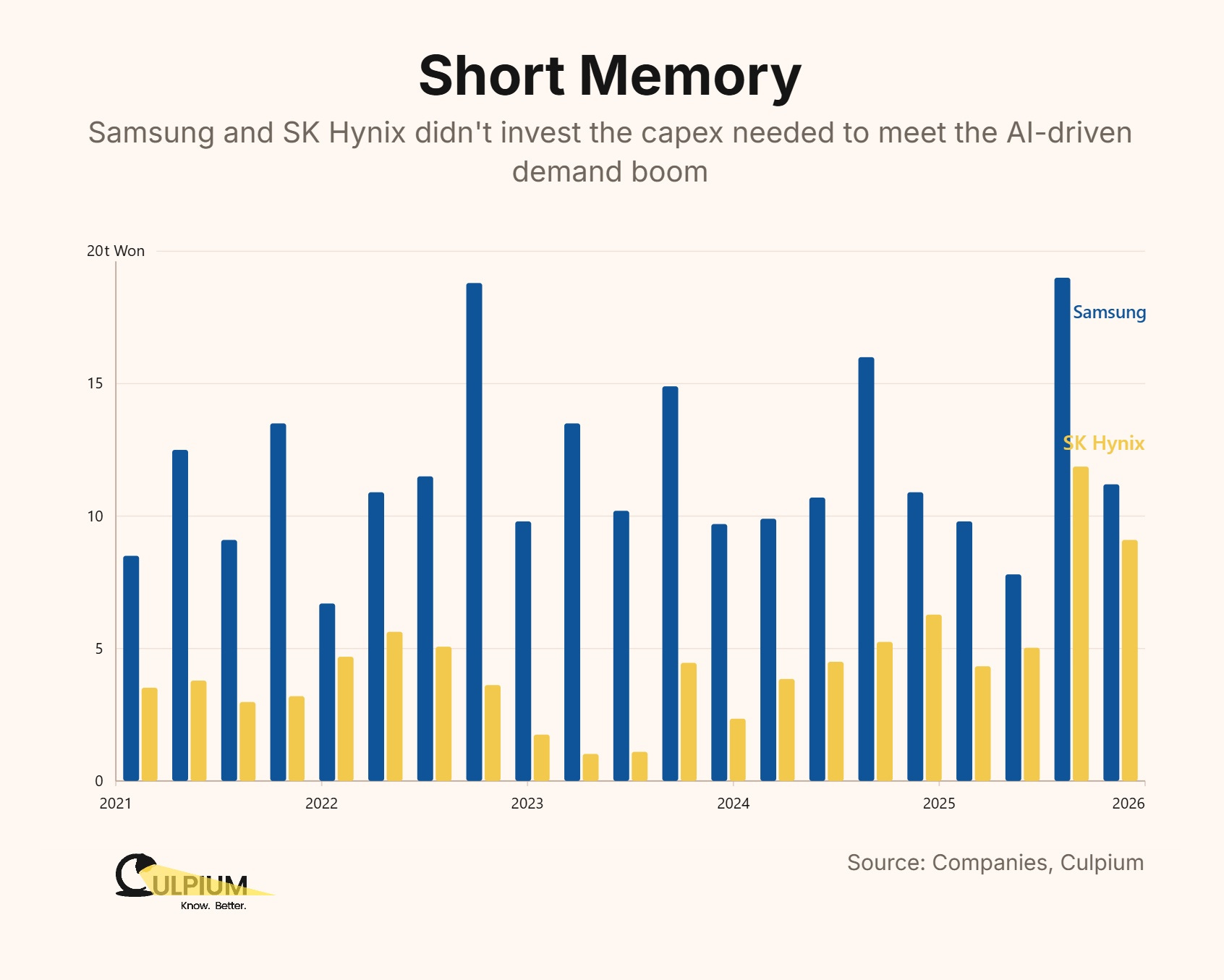

Samsung reported first-quarter earnings Thursday morning. What it revealed was great news for itself and fellow memory-chip makers but bodes very badly for everyone else.

Revenue at the South Korean company’s memory division doubled from the prior quarter as it started catching up to smaller compatriot SK Hynix in the lucrative market for high-bandwidth memory (HBM). Like SK Hynix a week ago, Samsung made all the right noises about HBM being important and its determination to boost supply.

Reading between the lines, though, it doesn’t feel like either company is taking the AI boom seriously enough, and they certainly don’t seem to care much about their long-time clients in the smartphone and computer sectors. At best, it looks like Samsung, SK Hynix, and US rival Micron are more intent on leveraging their pricing power than helping clients get the products they need.

Tune in to this week’s Supply-Chained with Tim Culpan (Culpium) & Jon Y (Asianometry).

Episode 2: Binning. An Old Nvidia Practice that’s Also Behind Sparse Supply of Macbook Neo

Witness SK Hynix’s first-quarter results. DRAM revenue, which accounts for 78% of its business, climbed around 65% while the average selling price also climbed around 65%.

SK Hynix didn’t sell more DRAM, it just charged more for it.

Samsung and Micron told a similar story. At Micron, whose latest quarter ended in February, ASP was up a mid-60s percent with revenue growth in the low-70s — its actual shipments, measured in bit-growth, barely budged. Similarly, Samsung’s DRAM revenue-growth tracked prices not output: ASP was up more than 90%, while shipments inched up just a few percentage points.

There have been loud complaints that TSMC didn’t expand enough to meet growing AI-driven demand from Nvidia, AMD, and cloud-service providers. But there’s been scant attention paid to the fact that these three major memory-chip suppliers collectively failed to either see, or take seriously, this historic moment.

I find that staggering, because I foresaw it three years ago.

“AI companies are likely to buy up more DRAM than any other slice of the technology sector in history,” I wrote in a previous life (gift link). “Established giants like Microsoft Corp. and newcomers such as OpenAI are set to pound on the doors of Samsung, SK Hynix and Micron”

That was back in May 2023, and over the past year this “pounding on the door” scenario has played out exactly as I predicted. And if I, a mere outside observer, could see what was about to happen then it’s impossible that executives at three huge semiconductor companies couldn’t.

Instead, what we’ve seen in recent quarters is management enjoying huge gains in revenue and profit without having to do the actual work of, well, shipping more product. The commodity nature of memory chips is such that when demand exceeds supply, prices quickly rise. The reverse is also true.

What’s worse, they’re all now crowing that this situation won’t end anytime soon.

“Amid this supply-demand imbalance, customers are prioritizing securing volume over pricing which is sustaining the current pricing strength,” SK Hynix CFO Kim Woo-hyun boasted last week. “Accordingly, we expect a favorable pricing environment to continue for the time being.”

Samsung was just as blunt about how desperate its customers are, and how the world’s biggest memory-chip maker plans to keep taking advantage of them.

“Unlike previous years, customers who are concerned about supply shortages are actually bringing forward their demand for 2027 already,” it said in Thursday’s investor call. “So, currently just based on pre-booked demand alone, the supply-demand gap is looking to widen further in 2027 versus this year.”

From a purely capitalistic point of view, I guess you can’t blame them. The memory sector is cyclical. You enjoy the growth years when you can, and limit pain of the down cycle when it comes. That’s the business model, and both management and investors have learnt to accept it.

Unfortunately, on this occasion customers are learning that they too must accept the vagaries of the memory industry. But it’s causing a lot of pain, will likely lead to billions of dollars in lost revenue, and hand more control to Chinese rivals just as global technology competition escalates.

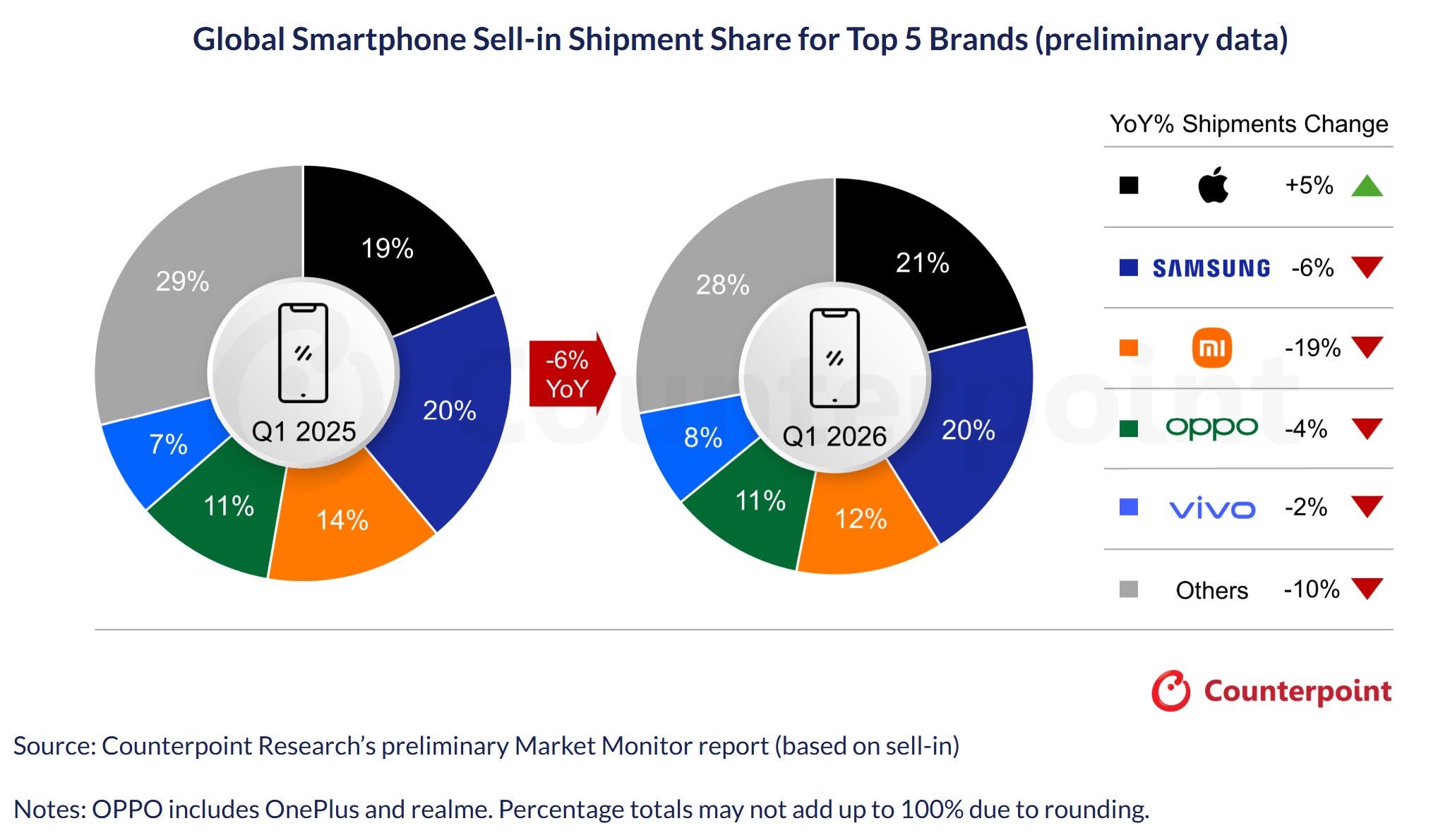

Worst hit will be PC and smartphone makers, who are having to rethink their product strategies given the long-term higher costs of both DRAM and NAND. We’re already seeing this play out.

All but Apple experienced a drop in first-quarter smartphone shipments, according to data from Counterpoint Technology Market Research. Xiaomi was worst hit, with a 19% fall.

“The brand is facing acute pressure as its heavy exposure to the price-sensitive entry-level segment makes it highly vulnerable to rising memory costs,” Counterpoint wrote of Xiaomi’s struggles. A delay in Samsung’s premium S26 series meant that even the Korean brand couldn’t stave off a downturn brought on by shrinking demand for mass-market devices.

Samsung’s smartphone chief addressed this issue in Thursday’s earnings call, noting the need to manage cost pressures and reorient toward premium devices over low-end models. I discussed this dilemma at length last week with Jon of Asianometry in our debut episode of Supply-Chained.

The PC sector will be similarly affected. Lenovo, which is number one with around 25% of the market, skews toward consumer and small & medium-sized business customers. That makes it potentially more vulnerable than HP and Dell who lean more heavily on larger corporate customers by selling both personal computers as well as infrastructure products like servers.

The three big memory-chip makers needn’t care. They have customers lining up for the next few years, many trying to lock in multi-year purchasing agreements. That’s given these oligopolists the confidence to finally start boosting capex, albeit too late and by too little.

But it’s not going to much help the rest of the tech sector, because most of that money is going toward boosting HBM supply used in AI servers, leaving those requiring legacy DRAM to flounder.

Boring old DRAM is needed in PCs, smartphones, games consoles, security cameras, cash registers, and cars. It’s boring because it’s ubiquitous. And it cannot be replaced by HBM because the high-bandwidth variant is attached directly to a processor via advanced-packaging techniques such as TSMC’s Chip-on-Wafer-on-Substrate (CoWoS). Legacy DRAM is often just soldered onto a printed circuit board and slotted into the final device.

The top three, which collectively control 90% of the DRAM market, may feel that they don’t need the old-school DRAM market anymore. But that’s very short sighted, because they’re handing orders and client relationships over to rivals in China, which threatens to take over the memory sector like it did legacy semiconductors and LCD display panels.

Whereas Western brands had become wary of buying memory chips from China, they now have no choice. Even HP, with its long-term No China policy, must turn to ChangXin Memory Technologies (CXMT), a growing player in DRAM and Yangtze Memory Technologies Co. (YMTC), which is now a force in NAND.

HBM may be the hot item now, but legacy DRAM will forever be important to the world because of its simple but critical role in how information is computed. The risk is that, as with other commodities like rare earths, China may soon have command of a critical product crucial to the global technology sector. Not that it’s Samsung, SK Hynix, or Micron’s job to care. Their job is to make money, not protect supply chains or national security.

Maybe Seoul, Tokyo and Washington might start to care, but given the current emnity between them all, I struggle to see their governments working together to effectively address the issue.

In the short term, those parts of global tech sector which are not building AI servers — which is most of the global tech sector — will continue to suffer. In the long-term, the entire tech sector may find itself facing an even worse problem than high memory-chip prices. Unless someone stands up and does something about it, before it’s too late.

Thanks for reading.

They're not doing this because they're evil. They're doing this because they can't predict if the current demand will reliably stay the same. The RAM industry has gone through multiple boom and bust cycles.

It's definitely true that advent of AI/LLM's represent a permanent qualitative change to society/economy, but to echo Yury the memory suppliers have deep muscle memory, scar tissues, whatever the best analogy is for the volatile boom/bust cycles which did as much to push other (mostly Japanese/EU) suppliers out of the market. They can invest now to expand capacity and then in 2 years when the capacity comes online they may find customers backing away from previous promises to help the investment pay off.

Furthermore, the most visible "end customers" for their own end-customers are the not-so-confidence-inspiring trio of Sam Altman ("podcast bro", as TSMC execs reportedly called him after Altman laughably proposed trillions for fab investments), Masayoshi Son, and Elon Musk.

With the move to IPO, we now have a much better measure of the WeWork-levels of incinerated cash by OpenAi and Anthropic (and most assuredly the smaller players as well). From my own personal experience, people who make a living from the manipulation of atoms are not as prone to the messianic fervor that often afflicts entrepreneurs in bits - note that the "tech evangelist" title is much less common at true hardware technology companies (they seem to be much more common in software and related internet/mobile, or consumer products, not stuff like IC's, as it is difficult to "evangelize" with a straight face about products that basically amount to applied material science)