Exclusive: TSMC Clients Handed Price Hikes Across All Advanced Nodes

[Exclusive] Price rises extend across 75% of TSMC's wafer-revenue base, deeper and broader than previously expected.

Good Evening from Taipei,

TSMC used its North American symposium in April to debut the foundry’s next process node and put memory-chip maker SK Hynix in the spotlight.

“This year, we are introducing derivatives of A14, including A13 and A12, both planned for production in 2029,” Kevin Zhang, TSMC’s senior VP of business development and global sales told the Santa Clara crowd.

Delivering the keynote, SK Hynix’s Head of Engineering Ahn Hyun outlined his company’s plan to build TSMC’s logic process into the base die of its HBM4 memory. “Let us become one team that shares technological progress in real time,” he said.

But behind the scenes — away from the spotlight and left off the presentation slides — TSMC was delivering another set of news to customers: brace yourself, we’re about to raise prices across multiple geometries.

Since early this year, business development and sales teams at TSMC have been told by senior leadership that they need to find ways to charge more, according to multiple sources I’ve spoken with in recent months. The Taiwanese foundry watched its memory counterparts enjoy higher prices and wanted in on the action, managers told them, according to my sources.

Tie those prices rises to TSMC’s value proposition and technical strengths, staff were instructed.

“The best piece of opinion writing I've read in a long time” — SOPA 2026 Award judges on Culpium’s nomination.

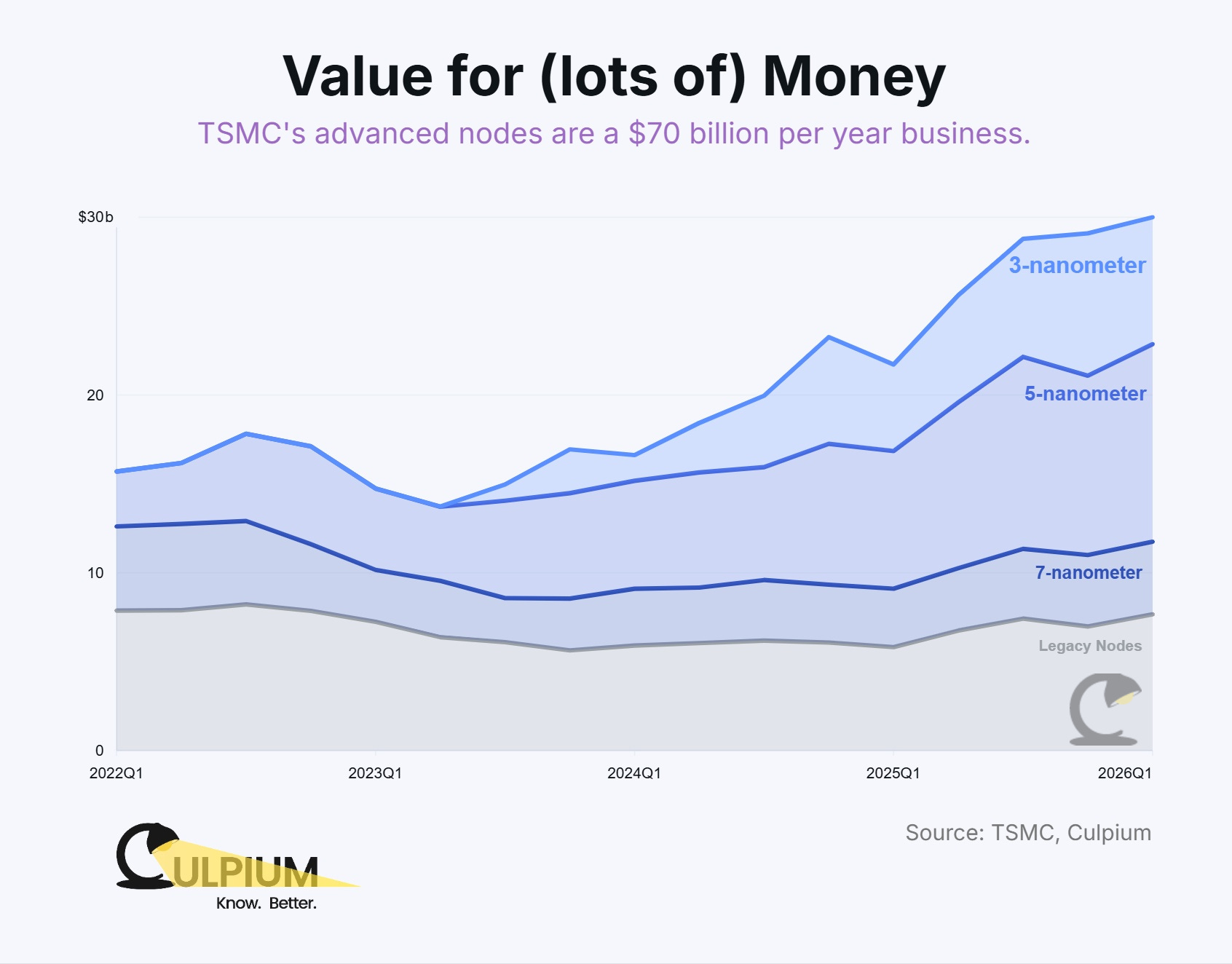

While rumors in Taiwanese local media have pointed to increases at the 3nm node, the reality is far more broad. All advanced nodes will become more expensive, that means 7nm and everything beyond it, TSMC told its clients.

That’s a three-fold expansion in the breadth and depth of the price rises that clients had previously feared. TSMC’s 3nm node accounted for 25% of wafer revenue in the first quarter, yet the entire advanced-node portfolio made up 75% of its wafer sales.

Supply-Chained: A weekly podcast by Tim Culpan of Culpium, and Jon Y of Asianometry.

“TSMC does not comment on pricing. Our pricing strategy is strategic, not opportunistic,” the company said in an emailed response to Culpium. “We will continue to work closely with customers and sell our value to them.”

Reading between the lines, I take that as a tacit admission. And it shouldn’t be a surprise that price rises would come. Earlier this month Chairman and CEO CC Wei told TSMC shareholders at its annual general meeting that he “would like to” raise prices. CFO Wendell Huang told the BBC the same day that he “does not rule out” price increases.

What caught some clients by surprise was these hikes being implemented even at the relatively older 7nm node — the first to deploy EUV lithography tools. What’s more, some clients believe TSMC will also jack up prices on some legacy nodes.

Price rises have already started rolling out, I am told. And even where they haven’t, clients have been instructed to build the higher cost structure into their purchase orders.

The exact scale of the increases has been hard to ascertain. I have been getting conflicting figures, which indicates the scale may not be uniform across clients, nodes and product categories, but they seem to fall in the 5% to 10% range.

Full-year revenue is expected to rise at least 30% to more than $160 billion in 2026, according to Culpium estimates. Around $85 billion will come in the second half, when the price rises kick in, and we can expect at least 80% of wafer revenue to come from advanced nodes. That means prices rises on close to $70 billion of sales, assuming a proportional increase in non-wafer revenue comprising around 15% of the total.1

Assuming an average 5% price rise, the hike could give TSMC a boost of 2 percentage points or more to full-year gross margin, according to Culpium analysis. Of course, that’s nothing compared to the price gouging being dished out by the memory makers. Samsung, SK Hynix and Micron jacked up prices between 65% and 90% in the first quarter alone, helping them raise gross margins by as much as double.

Clients may not love TSMC’s price hike, but at least they can pass it on to their own customers. As Tim Cook told the Wall Street Journal’s Rolfe Winkler last week, “unfortunately, price increases are unavoidable.”

Maybe those red Macbook Neos will arrive after all.

Thanks for reading

A footnote: Culpium once again won the silver medal (Honorable Mention) at the Society of Publishers Asia annual journalism awards in the Opinion Writing category. It’s a rare feat to be a finalist once, to do so in consecutive years is a greater honor. And we’ve only been going for two years! I plan to continue the pace of journalistic innovation and analysis. Your support allows me to keep doing so.

More from Culpium:

Price rises and margin boosts might carry over to non-wafer revenue, but such a scenario is not a given.

Very interesting and massive congratulations on your medal win!

I guess if I have a question it might be - is the TSMC decision a reflection of coping with historical manufacturing price increases? More to the point, once memory/component/equipment cost increase hit TSMCs own operations (as I presume they will now prices are set to increase) to what extent might it find it needs to raise prices again?