What SK Hynix's IPO Prospectus Doesn't Tell You

[Opinion] The world's second-largest memory chip maker has more stories than its F-1 filing reveals

Good Evening from Taipei,

SK Hynix is going big in America. The world’s premier maker of high-bandwidth memory is set to raise around $28 billion from a sale of American Depositary Receipts that will be listed on the Nasdaq this week.

Unlike compatriot Samsung which has a large suite of products, SK Hynix only makes memory chips: DRAM and NAND. As a result, this listing is a good chance for American investors to get exposure to one of the chief beneficiaries of the AI boom.

Rather than offer a lazy summary of the prospectus with screenshots and cliches, I decided to dive into data that isn’t immediately obvious. This includes a lot of information that is not even in the US-listing document.

An Announcement.

Culpium has been publishing free for almost two years, with a long hiatus in the middle. A paywall will go up in coming months. The price is $100 per year for those who pledge now. One week after turning on the paywall the annual subscription will go up to $140. If you pledge before then you’ll lock in that lower price but will not be charged until the paywall kicks in. I’ll give you a heads up when that’s about to happen.

Read this to understand Culpium and what I aim to offer.

I went independent so that I could give you exclusive, uncompromising, quality journalism. Please join me on the journey.

Subscribe if you haven’t already.

Pledge now if you’re already signed up.

Thanks.

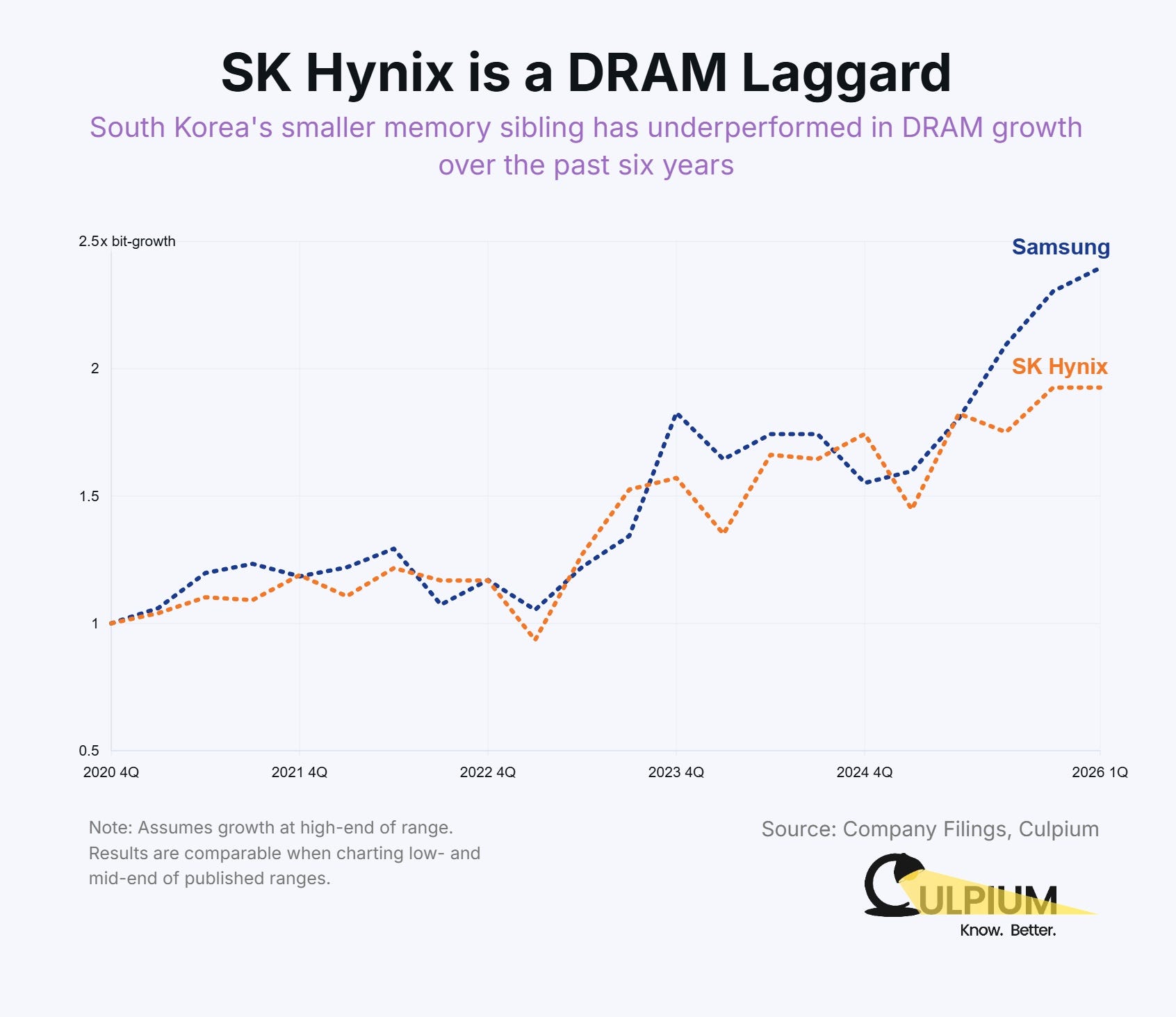

SK Hynix Has Been Slow to Expand

This is really counterintuitive, and something most folks don’t want to admit. But the numbers don’t lie.

Based on quarterly bit-shipment data provided by both Samsung and SK Hynix, I calculated just how much they’ve raised output since the Covid-led rise in 2020, through the 2023 downturn, and into the AI-boom sparked by the launch of ChatGPT in 2022.

Over that time SK Hynix’s compound average growth rate (CAGR) was around 11%. The gap to Samsung is particularly acute over the past two years when AI became such an obvious driver of DRAM demand.

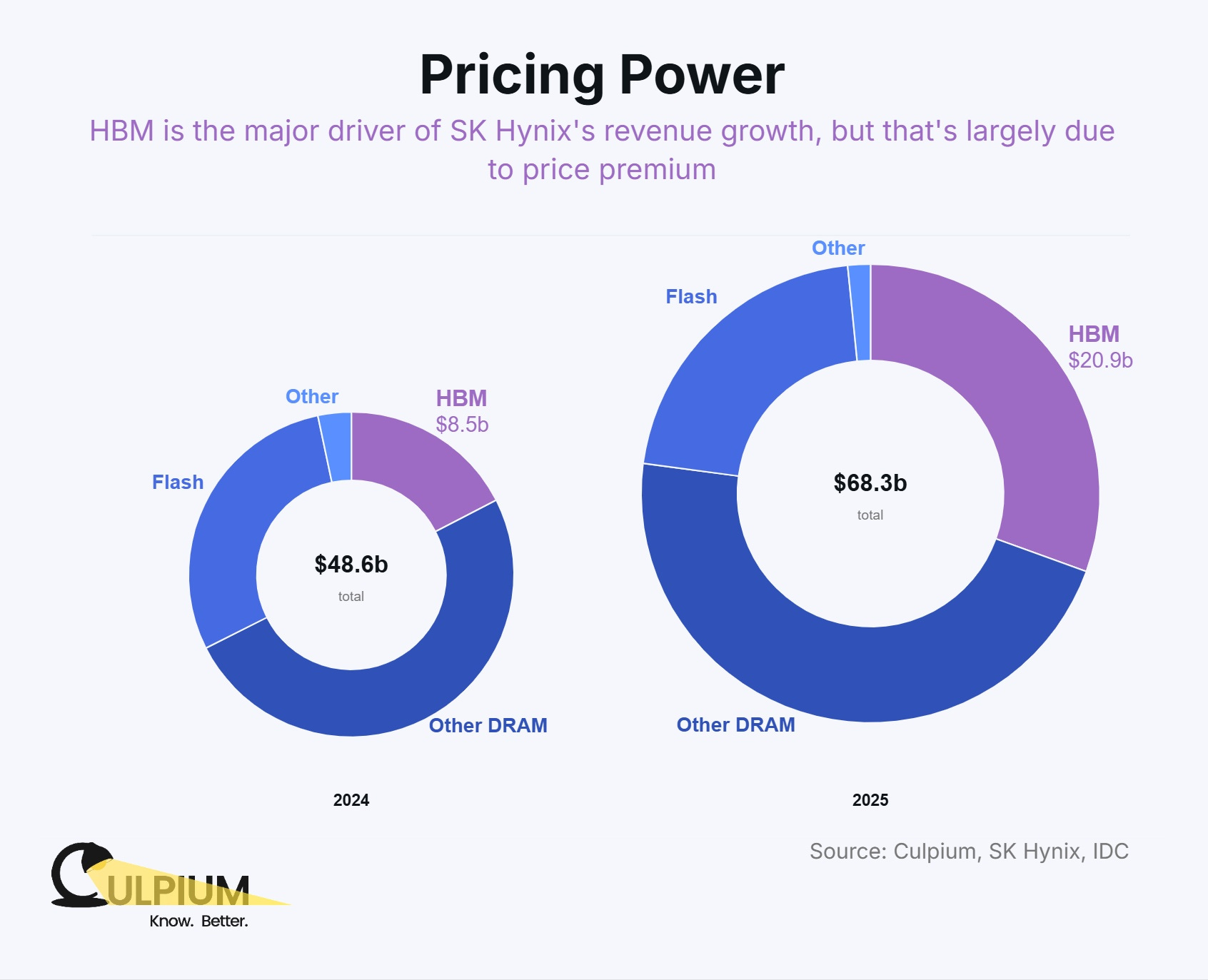

It is Highly Leveraged to HBM

Call it a bug, call it a feature, but let’s call it what it is. SK Hynix was the global pioneer of high-bandwidth memory when the others dared not tackle the myriad challenges that came with developing stacked DRAM which relies on advanced packaging.

Today, SK Hynix is rightly reaping the rewards for that R&D risk. HBM is 5x the price of standard DRAM when measured on a per-bit basis. The result is a massive jump in both revenue and profit margins.

Yet, by my calculations HBM accounted for around 8% of SK Hynix’s total DRAM bit-shipments last year and around 40% of DRAM revenue. At first glance this looks like low exposure, which it is. But given the massive price premium for HBM over standard flavors like DDR, this low exposure means high leverage.

Every bit of new HBM sales is equivalent to 5-bits of DDR revenue. That’s great when the market is growing. But when it slows, every 1-bit fall in HBM demand will have the same impact on revenue as losing an order for 5-bits of DDR.

Any analyst or investor who is modeling SK Hynix’s HBM as a competitive advantage in the AI boom must factor in this leverage. A slowdown in AI-chip demand could have a much larger impact on this company compared to Samsung and Micron.

Its Quadrillion-Won Plan Makes the US Look Small

American investors may be eager to throw money at SK Hynix. The love is not reciprocated. The US is its single-largest source of revenue at 69% last year, but the Icheon-based company has not, and will not, make America a significant manufacturing base. Less than 1% of its non-current assets — property, plants and equipment — are in the US.

A $3.9 billion plan to build in West Lafayette, Indiana is the company’s first significant step onto US soil. But that investment will barely the move the needle. The new plant will only provide back-end packaging, a low-value component of memory production, and pales in comparison to the 1.1 quadrillion won (yes, quadrillion!) SK Hynix has announced for Korean expansion over the next eight years. Even in USD terms — $710 billion — it’s a staggering figure which also shows that barely 0.5% of its capex is scheduled for American soil.

China Ties Will be Hard to Break

SK Hynix’s operations in China are deeper and broader than many realize. It makes both DRAM and NAND there, has a packaging & testing operation, and even a budding foundry joint venture.

Its position in China was cemented by the 2020 purchase of Intel’s NAND business. This included a Dalian NAND-manufacturing facility which has since been folded into its spunoff Solidigm unit.

Its headcount also tilts toward China. Around a quarter of SK Hynix’s global workforce is in China. The company even has a legal obligation to keep prices low in the country as part of a deal to get antitrust approval for buying Intel’s NAND business.

Health and Safety Concerns Persist

Some care, others may not. Either way, it is worth pointing out a few outstanding safety incidents including two which occurred as recently as last month.

In the latest accident, a fire broke out at its Cheongju plant which makes DRAM, including HBM. As a result, a gas leak occurred between fab M15 and its M15X extension resulting in the emission of toxic fluorine gas. At least seven people were affected and taken to the onsite medical clinic, local media reported.

Separately, a worker died last month after battling illness for at least 15 months. Details are murky, but according to the company the employee was categorized in March 2025 as suffering an occupational illness. Neither incident was mentioned in the Nasdaq IPO prospectus.

Generally speaking, semiconductor manufacturing might be considered a low-risk occupation for workers. But numerous noxious chemicals are used, and when accidents happen serious injury and death has been the tragic result.

Thanks for reading.